There are two phases in the RRSP life time: the accumulation phase and the withdrawal phase.

Accumulation phase

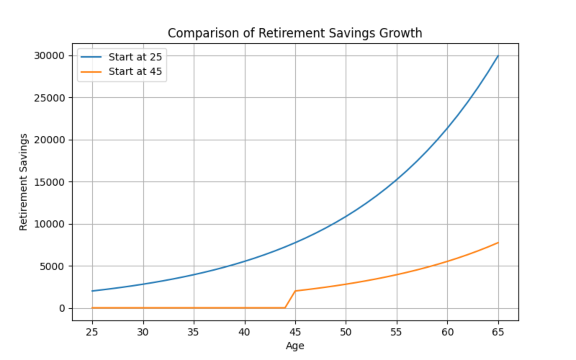

Dynamic growth with a constant savings habit that profit from compund interest

Contribute early and regularly:

The earlier you start and the more you persevere, the more compound interest works for you.

Invest strategically:

Choose your investments based on your risk profile and goals.

Save on taxes:

Your contributions reduce your taxes and you can reinvest tax refunds.

Financial tip:

Talk to your accountant at the beginning of the year to know your RRSP contribution room. Do not let this conversation for the last minute, you might miss the deadline to make contributions.

Talk to a security financial advisor to better understand the two RRSP phases considering your current life situation.

Withdrawal phase

Using your savings as income in your retirement

Plan your retirement

Consider longevity, the age you would like to stop working and the lifestyle you wish to have at this stage.

Withdraw strategically

Think about making small withdrawals and the tax impact they will have on your income tax.

Complement your income

Your RRSP works alongside government programs and employer pensions.

What is the difference between an RRSP and a TFSA?

RRSP contributions reduce your taxes now, but withdrawals are taxed later. TFSA contributions don’t reduce taxes today, but withdrawals are 100% tax-free.

How much can I contribute each year?

Up to 18% of your previous year’s earned income, capped by the government (e.g., $33,810 CAD in 2026). Unused contribution room carries forward.

What happens if I withdraw before retirement?

Withdrawals are taxable, except under special programs like the HBP or LLP (Lifelong Learning Plan).

Can self-employed workers open an RRSP?

Yes, RRSPs are available for self-employed individuals as well.

What do I need to open an RRSP?

• Valid ID.

• SIN (Social Insurance Number).

• Proof of income.

• Bank details for automatic contributions.

Clientes que hoy disfrutan su retiro con seguridad y planificación

Publié sur Google

Olga Canelas

29/10/2025

Trustindex vérifie que la source originale de l'avis est Google.

Rated 4.5 out of 5

Adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua ut enim ad minim. of high value and temperature sensitive loads monitored times.

Co Founder

Jhon william

Rated 4.5 out of 5

Adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua ut enim ad minim. of high value and temperature sensitive loads monitored times.

Co Founder

Sarah albert

Rated 4.5 out of 5

Adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua ut enim ad minim. of high value and temperature sensitive loads monitored times.

Co Founder

Mike hardson

Learn more about savings and investment strategies in Canada

FINANCIAL TIPS TO BUILD YOUR RETIREMENT STEP BY STEP

Financial security

The 3 mistakes that keep you from achieving financial stability (and how to avoid them)

Discover the most common financial mistakes and how to fix them so you can build lasting security and economic well‑being in Canada.

Life, Disability or Critical Illness Insurance: Which One Do You Really Need?

Discover the differences between life, disability, and critical illness insurance. Learn which one fits your situation best and how to protect your financial security in Canada.